![]() RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

SO, WHAT NOW?

The way things stand right now, in the financial and investment world, everyone is asking, WHAT NOW? This is a very tricky time and being “long cash” could potentially be a risky move too. There is a definite risk to buying or holding onto any asset class. It is unclear whether US equities are out of a bear market and at the start of a new bull market. Currently (mid-April 2023), despite the inflation indicators (CPI, PPI) moving lower, investors are nervous about an “upcoming recession” towards late 2023. There is nervousness regarding future earnings contractions (lower EPS) and worry about upheaval in the banking sector. The main focus of this write-up is applicable to investible amounts with a holding period of 3+ years. During the 2022 bear market, the S&P 500 traded in a range of 3,500 – 3,900 for around 6 months and the “bottom”, around the 3,500 mark, was tested multiple times. It is possible that the bottom of that bear market was reached during H2 2022. From here (April 2023), the market may still have a pullback from its current 4,100 levels but that could be 10%+/- and that would still keep the S&P 500 above the previous “floor”. The prior peaks reached during 2021/2022 had a huge contribution from “big tech” stocks and had significant PE multiple expansion among the mid and small caps. The current growth in the indexes is actually related to defensive stocks such as large pharma, utilities and the current PE ratio is around 22.0x from 18.0x in Q3 2022 (around the potential bottoming process). These multiples by no means demonstrate “over valuation” for US equities. Hence, there is a good chance for the indices to rise going forward. Assuming that we may either be at the end of the current bear market or at the start of a new bill market is prudent.

At this time, it would make sense to be long/ buy US equities but being selective matters. The pharma/ large biotechs, the beaten down large techs, the large financials, dividend stocks/ ETfs, the “winning” mega cap retailers and the 3 major indices would be potential and logical LONGs. The large pharma sector has also shown some separation where there is a group of large pharmas and biotechs that are outperforming the rest of the sector. The stock prices of the previously richly valued big techs have been battered and these companies are restructuring their business. Hence, they are poised for price growth going forward. The large financials had price contractions during the recent “bank failure crisis” and the financial sector may now be more stable going forward. ITS VERY IMPORTANT TO BE SELECTIVE IN EQUITIES AND BE LONG ONLY THE HIGH-QUALITY NAMES.

It is very probable and possible that US residential real estate prices will further soften going forward, there is a strong possibility of a 20% or so decrease over the next 24+months but one does not foresee the same violent crash in prices like in 2008. This could create buying opportunities in the future and the start of a new bull cycle thereafter. At this time, it would be prudent to be long/ hold a “core portfolio” which has a good income stream. Risky real estate assets in Tier 2 or Tier 3 US cities could be sold to lock in some gains. It may not be prudent to add new assets at this time in Tier 2 or Tier 3 cities. Purchasing residential assets in Tier 1 US cities could have merit. Overall, it may be prudent to wait and watch for at least the next two quarters or so.

Commercial real estate is a different asset class and is not being referred to in this analysis. Offices, hotels, retails spaces are a riskier asset class when compared to residential real estate and hence from time to time have better returns. But, overall, these assets are best left to “professional REITs”. Volatility of these markets is not for regular HNIs and with increasing interest rates and risk of recession, these assets harbor significant downside risk. Fixed income assets could also be a problem if the Fed continues to raise rates, since prices could come down. However, if the Fed stops raising rates or cuts rates then that would work positively. Being exposed to high quality Fixed income assets like treasuries or high-quality corporate bonds is sensible. Buying treasuries with inflation protection features (TIPS) would be among the most sensible things to do.

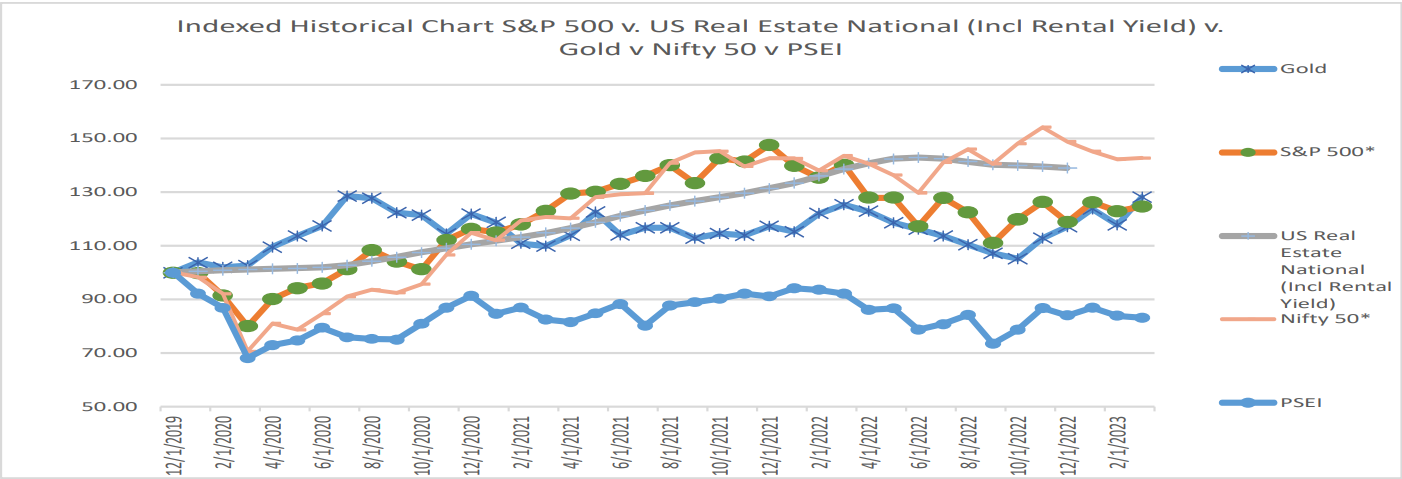

The Indian equity markets, at this time, are trading with the Fed behaviour in focus. High quality Indian equities provide strong growth dynamics and diversification for any portfolio. Hence, it is beneficial for a portfolio to own/hold the large cap, historically widely held Indian companies with proven management teams and the main index ETFs. Mumbai residential real estate may not still be at the cusp of a new bull market, especially since rates are rising in India. A certain exposure to a high growth emerging market like India may be sensible if its part of an “overall strategy”. South East Asian equities and real estate (Philippines) could be a risky bet at this time, if there is a position then holding onto it is fine, but adding new positions should be done only on a case-by-case basis.

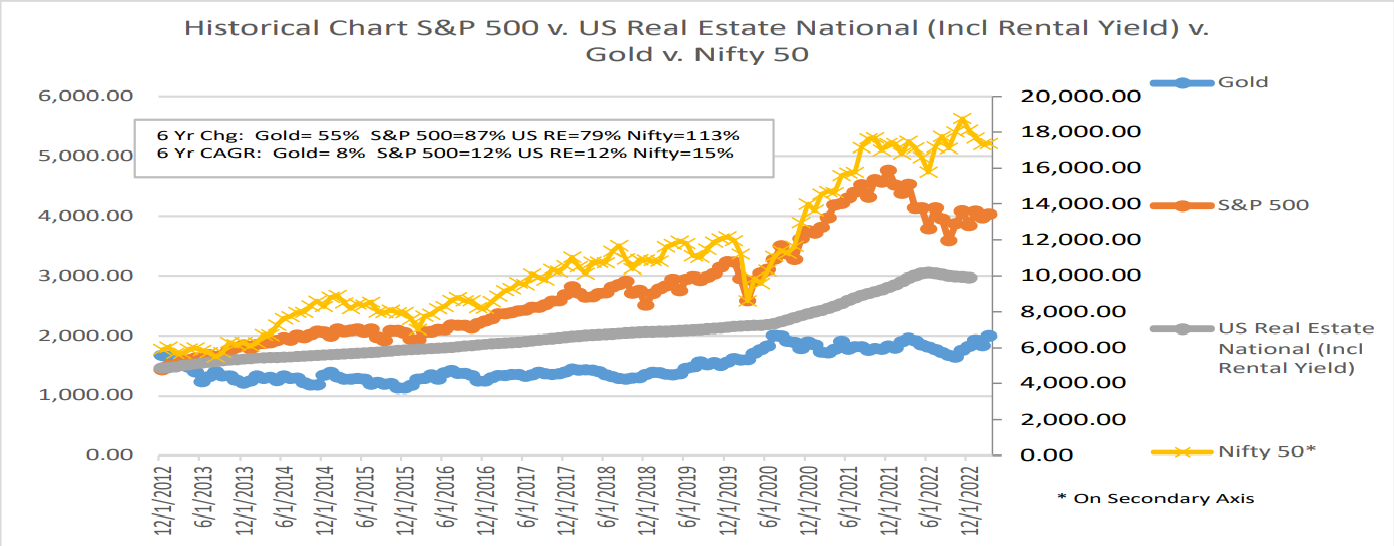

Gold is at a “life-time” high and is still rising, inflation, recession and other types of macro risks are beneficial to gold. A small part of any HNI portfolio should include a position in gold. Holding onto some cash to take advantage of any future opportunities is important.

WHERE ARE WE WITH INFLATION?:

As of Q2 2023, the global economy is poised at a cross-road, the Fed is potentially, as believed by many market participants, towards the end of its historic rate tightening. From March 2022 to March 2023, the Fed has enacted nine rate hikes: 3 of 25 bps, 2 of 50 bps and 4 of 75 bps. Since 2022, the Fed announced that it would prune its balance sheet by about $95 billion/month ($60 billion in Treasuries and $35 billion in Mortgage Backed Securities, MBS). This was in response to historic global inflation. Inflation for 2021 and 2022 was approx. 7% and 6.5% over the previous year and were the highest inflation rates since the 1980s. Inflation rates hit almost 9.0% in the middle of 2022. The March CPI was released on Apr 12, 2023 and seemed to demonstrate that the rate hikes were serving the purpose of cooling down inflation but the market was still evaluating whether this is a “temporary, non-linear event” or is it demonstrative of a downward trend. Hence, the market is trying to guess how the Fed will react in respect to the rate hikes in May 2023 and beyond. The causes of this historic inflation have been well documented and discussed and were partly the result of the historic pandemic era monetary and fiscal policies. The Fed is attempting to engineer a “soft landing” of the economy to bring down inflation. The current unemployment rate is around 3% and the Fed believes that an increase in the unemployment rate by 1.0% would ease the inflationary environment in a stable and meaningful manner. Investors worry that all these factors could induce a US recession in H2 2023, Q1 and Q2 2022 had negative GDP growth but due to the “strong labor market” that was not considered as a “recessionary environment” and strong inflation readings continued. Soft landing and a short recession are what the Fed is hoping to achieve to tame inflation but that comes with risks.

The ECB is also raising rates across the EU and currently the bank’s main rate is at 3.0% from negative rates until July 2022. In India, the RBI has been increasing Capital Reserve Ratio and the Repo rates, Repo rates were being raised by 25 bps and 50 bps at various times during this time and the current Indian Repo Rate is at 6.75%. This has resulted in increased interest rates across fixed income markets too. There may be chance of further tightening from the RBI and thus inducing fears of a recession in India.

Gold prices have been moving up and as of Apr 2023 are close to $2,000/ ounce. Bitcoin and Ethereum prices are also moving up and are close to $30,000 and $1,900 respectively.

WHERE ARE WE WITH THE STOCK MARKETS?:

As of Q1 2023, equity, fixed income, gold and oil markets (including others) are experiencing unprecedented volatility. The fall from the highs, for equities, reached in Q4 2021 and Q1 2022 has been rapid. By Q1 2023, all the US indexes are down when compared to the highs reached in 2021/2022, the Dow Jones and the S&P 500 are down around 14% while the Nasdaq is down around 24%. The sell-off intensified in H2 2022 but in Q1 2023, the markets attempted to rebound to some extent. By March 2023, the indices stabilized and started moving in a positive direction because the market started thinking that the “contagion risk of bank failures” had been quelled for now and the Central Bankers had a grasp of the situation. The Nasdaq is up around 15% and the S&P 500 is up around 5% for Q1 2023 from Q4 2022.

The bounce from the Q2 2020 lows, for equities (covid related), had been meteoric and rapid. By Q4 2021 and Q1 2022, all US indexes were at or close to all-time highs. The recession of 2020 was the shortest on record and historic government intervention prevented an economic collapse. But, in 2022, Fed tightening (rate hikes), the inflationary environment, Russia/Ukraine war and uncertainty in the Chinese cities due to covid related restrictions created major risks for risk assets. And these factors have resulted in equity bear markets when compared to previous highs. As of year-end 2022, the Nasdaq was down almost 30%, S&P 500 down more than 17% and the Dow down around 15% from the start of the year. US equity markets have moved up in Q1 2023.

In India, the equity markets have pulled back from highs reached in Q4 2022 but are currently rebounding. The markets pulled back around 7% from the highs. The effect of the Fed tightening on the overall global economy and emerging markets is a genuine issue. This has had an adverse impact on the Indian Rupee and the USDINR is at an all-time low. Further in Oct 2022, the Indian markets hit life-time peaks and hence valuations have become more reasonable. India also faces headwinds from oil pricing. Most currencies and particularly the Emerging Market currencies have been adversely impacted by the Fed tightening, the USDPHP and EURUSD, among many, are at their life-time lows. The Euro briefly came to parity with the US dollar in 2022.

WHERE ARE WE WITH THE REAL ESTATE MARKETS?:

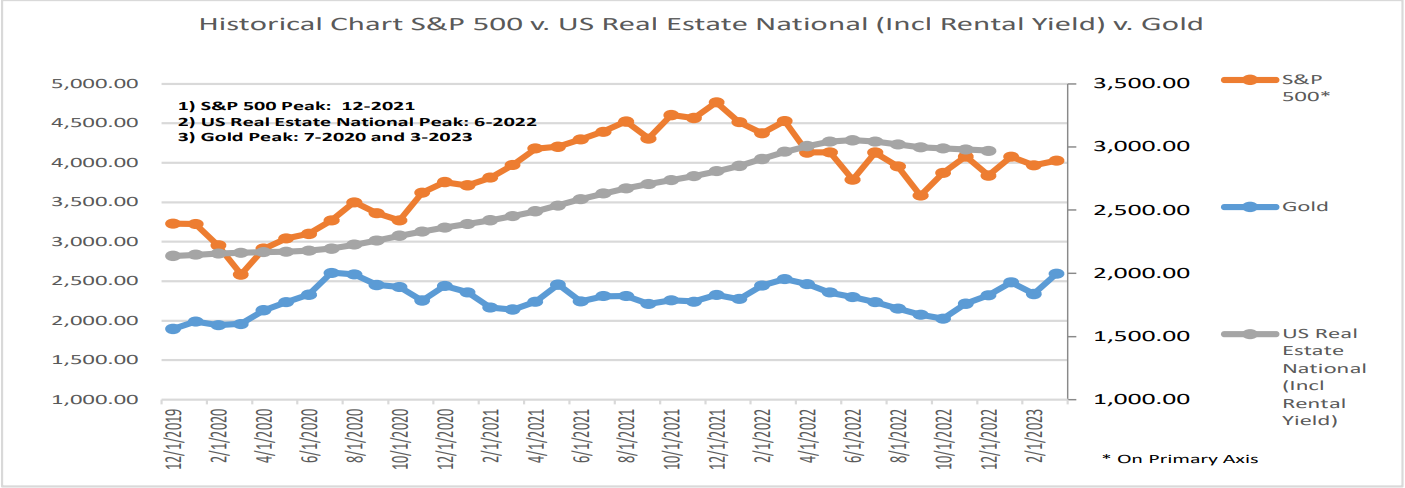

The bursting of the US real-estate bubble, in 2006, created opportunities for investors till about 2014. But the current pricing poses downside risk with potentially peak pricing reached in 2022, at least for the “near-term”. The US real estate cycle typically runs for a 10–12-year period and the current upswing started in 2012. One could say that the prices have risen too much and too quickly in many US real estate markets since the start of the pandemic. Additionally, rising interest rates are impacting mortgage rates and as of March 2023 fixed rate mortgage rates touched 6%+. As of March 2023, 10-year Treasuries were yielding close to 3.5% and there have been multiple instances of yield curve inversion over the last 24 months. There is softening in the residential real estate markets in the US, after markets hit potential “peaks” in Q2/Q3 2022. The rate of price growth is decelerating and the slowdown has started in previously “red-hot markets” in the West, like Phoenix AZ and Las Vegas NV. Markets in Florida like Tampa and Miami are still showing “signs of growth/ appreciation” but it seems the markets are at the end of the cycle and the slide that started out West will catch up soon. At this time, demand is still strong in the residential real estate markets but affordability is a major limiting factor especially for first time buyers. Supply chain disruptions and inflationary price pressures for building materials and labor shortages are somewhat easing and this will positively impact the supply of new residential real estate. The potential fear of decelerating prices, while current prices still being “high”, may result in increased number of potential sellers going forward. Prices are now moderating even in many southern / south west / south east markets, prices in Houston and Austin TX are now coming down and sellers are employing price cuts to be able to effectively market their properties. Housing starts/home ownership statistics are increasing while buyer demand was at historic levels. There is still a significant work from home component and this potentially could create significant risks for office real estate.Interest rate risk (due to Fed tightening and supply chain disruptions) pose risks to both real estate and equity.

Another important trend in residential real estate is weakening of rental growth across various markets. Rents are coming down across many urban and suburban markets in the US, both in terms of increased promotions for tenants and lower rent amounts or rent hikes, for renewals, being charged by landlords. The pandemic shifted buyer preferences towards suburban areas and southern states, with lower cost of living and larger homes, compared to densely- populated urban areas. But that changed H2 2022 onwards, as corporates are now going back to pre-pandemic practices, including asking employees to return to the office. The global health crisis, the economic fallout and the weak fiscal and healthcare response from most emerging (previously fast growing) Asian economies has affected their growth trajectories.

Real estate prices in Mumbai have been declining for around 6 years and recently the government decreased registration costs to provide support. Mumbai real estate has been showing some positive momentum since late 2021 but this appreciation is not material when compared to the losses incurred since 2015.

Philippines had been hit hard by the virus and its vaccine response had been less than desirable. Manila real estate prices contracted in 2021, the first time in many years. Rental rates have also been hit and vacancy rates shot up in Makati in H2 2021 because many residents moved to the provinces. However, in 2022, that’s been changing and people are moving back into Makati and hence vacancy rates are now coming down and rentals are again getting occupied albeit at lower rates.

CONCLUSION:

HNIs with an investment horizon of 3+ years could take advantage of the current environment and be selective in making new investments or holding onto current investments, as outlined. Taking profits of riskier positions, for the current scenario, is always an option. However, all this is very relative and personal dynamics for an individual could always overrule any analysis provided.