![]() RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

Residential Real Estate Path–Where Do We Go?

Real Estate Markets Trajectory?

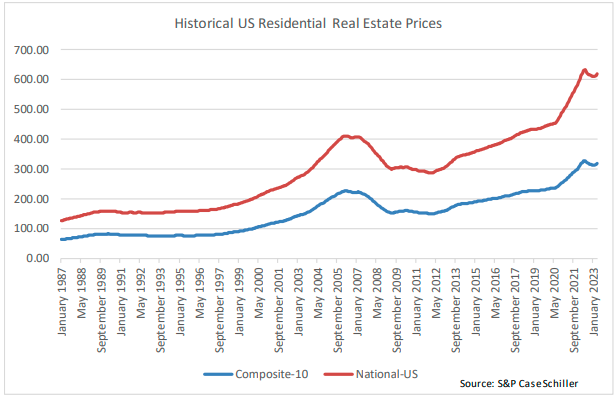

Residential Real Estate has weathered the storm, till now! Since 2020, residential real estate has rebounded, some may say, too quickly and gone too high! Most US residential prices are now at or close to lifetime highs. Almost all US residential markets are currently at their lifetime highs or have seen lifetime highs between 2020 to now. Most of the markets that had been part of the “2008-bubble” and its subsequent burst are about 60%, on average, over its 2000-2010 highs. Most of the real estate markets, outside of the Midwest, peaked in mid-2022. But, the current prices are not too far from those lifetime peak housing prices and most markets are less than 10% away from those 2022 peaks. These dynamics on its own could mean that a slowdown in prices could happen, but it is “riskier” against a backdrop of the current inflationary environment and Fed rate hikes.

Since 2022, the Fed has been taking unprecedented QT (quantitative tightening) action to curb the post-covid inflation problem. The current Fed Funds rate (June 2023) is 5%-5.25% while annual inflation in May 2023 was around 4% and in the downward direction. The Fed had enacted 10 consecutive rate hikes since March 2022 with its first pause in June 2023. The rates were increased from 0%-0.25% to current levels. Fed funds rates have impacted various treasury rates which in-turn impact mortgage rates. Mortgage rates, 30-year fixed, currently are in the range of 6%-7% which is high when compared to rates from 2008 onwards. But, these rates are not too high when considered in the longer-term historical context. The mortgage rates in 2020 and 2021 were low, in the range of 3%, because of the pandemic era Fed easing. In the last 12+ months, mortgage rates have almost doubled while real estate prices have adjusted marginally downwards, as expected. The residential real estate prices have weakened since the hikes started but this down move has been subdued.

Lifetime Peaks and what that means?

The first market to hit a lifetime high was San Francisco, around March/April 2022. This somewhat coincided with the peaking of the equity markets around end of 2021 and Q1 2022. The faster growing Tier 2 and Tier 3 markets, like Phoenix, Tampa, Miami, Las Vegas, Seattle etc and Tier 1 markets like New York peaked by around Q3 2022. The rate hikes started at the end of Q1 2022 and their effects have been permeating through the markets. Lifetime peaks of most US markets, except in the Midwest, were between 50% – 100% higher than the peaks reached during the 2006 bubble years. As the mortgage rate increases permeate through the system, real estate prices have started weakening but have not fallen off a cliff. That’s an important indicator of the resilience of the residential real estate market.

Past Rate Hikes

Rate hikes do affect real estate prices negatively but, in most cases, regulators tend to strike a balance and hike rates to a point where the exercise doesn’t “destroy real estate prices”. Interest rates had been hiked by regulators from 2015-2018 from 0%-0.25% to 2.25%-2.5% (by 2.25%) which resulted in mortgage rates (30-year fixed) increasing from 3.5% to over 4.75% but that did not hurt the then real estate price increases. From 2004-2006, interest rates were hiked from 1.25% to 5.25% (by 4%) and mortgage rates rose from 5.5% to 6.5% but real estate markets peaked during this time, to the point of being a “bubble”. Hence, historically it’s evident that real estate prices can withstand reasonable rate hikes. Another effect of increasing mortgage rates is the decrease in the number of potential home-sellers because people that have locked in lower mortgage rates are reluctant to buy “higher priced” real estate at current high mortgage rates. The trade-off is financially not attractive/ unaffordable and the monthly mortgage payments would balloon too much from current levels due to a “double whammy”.

Non-Price Data

It is safe to assume that the US housing market is currently undersupplied. Housing starts are going up in the West and the South but still below highs reached a decade or so ago. In the Northeast, the housing starts are going down. The Current FRED months’ supply is increasing and is around 8 months or so but is still low overall. The FRED existing home sale number is going up but is still significantly below levels since 2019. Rental vacancy rates and Homeowner vacancy rates are at historically low levels. Rents in most parts of the country are close to historic highs, albeit coming down. First time home buyers are strained, in terms of affordability. All these indicators together definitely create a supply constraint on real estate for sale.

CONCLUSION:

Currently, real estate prices are coming down. This down move started in the west and was moving across the country. Over the last few months, prices have been either flat or increasing slightly in the south east and the north east. By, traditional measures on an average the residential real estate market experienced close to a correction over the last 12+ months or so. However, residential real estate prices are still at or close to lifetime highs. It seems increasingly unlikely that residential real estate will experience a 2008 like price collapse. So, on an overall/ generic level (understanding that local real estate markets may have differing dynamics) it may be prudent, currently (6-12 months), to hold off on buying investment real estate (residential) even though longer-term real estate is an attractive investment option. If one has a “core residential real estate portfolio” which generates income then holding onto the “core” portfolio makes sense. It is definitely not a bad idea to book gains on real estate that is not part of a core portfolio and that one might own in riskier markets. The probability of real estate assets having out-sized gains over the next few years is not high.

Further, there are definitely chances of other assets classes outperforming real estate over the next few years. There is a good chance that equity markets could be at the start of a new bull market after suffering through a significant pullback through 2022. In contrast, real estate prices barely decreased and are hardly “a bargain” at this time. Making a fresh residential real estate purchase can be avoided at this time (6-12 months), but if undertaken, due to some compelling reason, then the leverage should be reasonable.

Buying or selling a HOUSE TO LIVE IN is a completely different matter and is based on individual needs and follows a different decision tree. That is NOT being discussed in this piece.

Commercial real estate is a different asset class and has many sub-categories. Some categories like retail, hotels and office REITs are showing signs of stress while other categories like warehouses are not. Commercial real estate is not being discussed in this piece.