![]() RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

How many times has one heard “Mumbai real estate never goes down”? People say this emphatically and seem convinced. However, it really is their “thought”. Many global real estate markets with more depth, larger capital pools and broader investor base have had downturns. So, why NOT Mumbai? AND it has happened in the past.

Your House Is a “House”: I believe real estate falls into two categories: 1) Property for Use and 2) Investment Property. Most people confuse their residence/office as an “investment”. Nominal prices may have appreciated during owner occupancy. However, its monetization would be disruptive and would need suitable substitution. In the US, families typically own large houses during child-rearing years. Once children leave, couples down-size and unlock the “equity in the house” for retirement. This does not happen in India and “locked” wealth has no direct benefit. So, property “for use” should be viewed as such. Owners should buy the best home/ office within ones affordability parameters.

Risk Is Key To Investing: The basic premise across asset classes is “wealth generation”, either as capital gains or as an income stream. Asset evaluation is in context of risk/return, “risk-adjusted returns” are key. Investment property, like dividend paying stocks, provides both income and capital gains. Real estate investing is highly amenable to leverage, when employed judiciously but over leverage increases risk.

Valuation (Price) Matters: Valuing investment real estate involves analyzing price/annual net rent, capitalization rates (annual net income/price), past annual capital gains (real/nominal), affordability of a wide group of buyers, among various metrics. Relative/comparative analysis of “value” with other similar priced real estate is critical (both local and international). Like any asset, overpaying for real estate is detrimental.

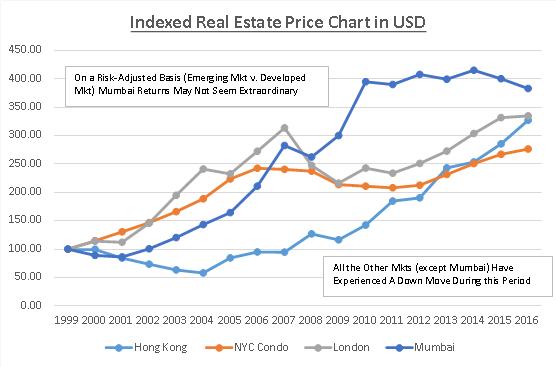

Comparing Mumbai To Other Markets: Based on my research, I believe, currently real estate in Mumbai is overvalued. Sales Price/Annual Net Rent, (developed market fairly valued property), is around 10.0x-22.0x. Currently, real estate in NYC trades at around 25.0x and there is talk of NYC real estate going ahead of itself. While in Mumbai (south and central) this same ratio (conservatively) is 40.0x+. Many argue that Indian assets command valuation premiums because of India’s phenomenal growth rates. The question is what “premium” justifies the current growth rates? India is an emerging market and higher returns generated here compensate for the higher “EM risk premium”. On a risk-adjusted basis, NYC real estate looks better. Reasons include pricing/process transparency, fair/timely legal system, stable regulatory system and superior product quality. In Manhattan $450,000 buys 400-500 sqft while Rs. 3 crores buys around 650 sqft (carpet area) in south/central Mumbai.

Net rental yields in NYC and Mumbai are at 2%-3% p.a. Lower yields require compensation through high capital gains CAGRs. US mortgage rates (30-yr fixed) are at 4% p.a while shorter term Indian mortgages are at 9%+ p.a. Previously, Indian mortgages had double digit interest rates. So, the hurdles for Mumbai’s returns should be higher.

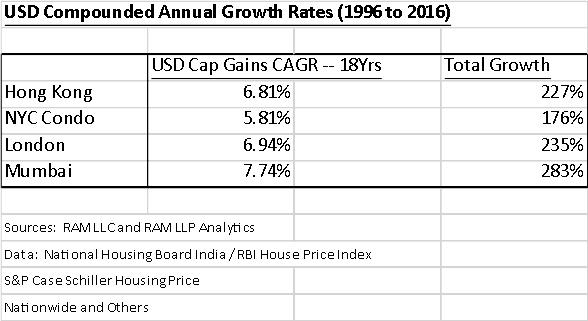

The CAGR for Mumbai real estate (Total Returns) from 2010 to now is around 7% (India annual inflation approx 6%). The CAGR of NYC real estate during the same period is around 6+% (US annual inflation approx 1.5%). Over a longer period, 2000 to now, CAGR for Mumbai is around 12% while for NYC it is around 6%. However, NYC corrected down 30% from its peak during the “bubble burst”. NYC condominium prices passed the values reached during the peak (2006) in 2016. Mumbai is at peak pricing or close (it may now be on the other side). Additionally, the INR has depreciated by 30% from 2008 levels against the USD. This further dents dollar based returns of Mumbai real estate.

Affordability is a key criterion where Mumbai pricing makes no sense. In an efficient market, there are multiple “types” of buyers and sellers. Mumbai is full of super-rich businessmen investors turned landlords. In NYC, a corporate employee, 3 years out of grad school, can buy a starter apartment. In Mumbai, even senior executives cannot buy starter apartments in South and Central Mumbai, on a stand-alone basis. NYC has replaced London as aspirational real estate and has generated significant foreign investor interest post-Brexit. Mumbai has a local investor pool.

Mumbai Needs a Price Correction/Stagnation: Every standard valuation parameter demonstrates Mumbai real estate as overpriced. Unless rents move up dramatically (quite unlikely) the way to revert to mean is — price correction. Prices could correct through a single hard hit (“shock to the system”) or by meandering for a few years. Flat Mumbai pricing since the last 3 years demonstrates stealth losses for owners (high Indian inflation /FD rates). A positive for Mumbai is that global cities/metros (except Tokyo — late 80s/early 90s) bottom out -25% to -30% within 5 years +/- from established peaks.

Signs of a Slowdown Abound: Sales are slowing down to a trickle, inventory is piling up and developers are cutting prices indirectly. Developers are now offering indirect discounts such as paying registration fees, not charging “floor rise” and rationalizing payment slabs (majority funds due at possession). Another myth, in my opinion, is the “scarcity of space in Mumbai” argument. There are enough dilapidated structures in the city which if zoned optimally would result in significant inventory and thus would create a rationalization of pricing.

Demonetization—A Major Item: All this is without factoring “the effects of demonetization”. Demonetization should impact Mumbai real estate (mostly negative) because of the cash component in Indian real estate purchases.

Interest Rates: Compared to western countries real estate prices in India are not “highly” correlated to interest rates. Indians use less leverage while making real estate purchases. Also, 1% change in mortgage rates results in smaller monthly payments but the “small savings” are immaterial when stratospheric prices abound.

Clearly, real estate in Mumbai is overvalued in the short/medium term. But long term, it will exhibit good growth rates owing to the growth potential of the Indian economy. The implementation of Real Estate Regulatory Act and the recent Budget change of long term capital gain reduction to 2 years for immovable assets could have a positive effect in the long term.