![]() RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

How Does One Navigate This Market?

Tricky Situation Across All Asset Classes

We are currently in an investment situation which is challenging but positive. The overall outlook of the macro-economies the world over is optimistic though not without risks. Many asset classes are priced at or close to “all-time highs”. In such an environment putting “new money” at risk is difficult, it is challenging to manage the money currently in risk assets and manner/amount of profit taking becomes tricky. Professional fund managers cannot sit back passively and leave “money” on the side-lines but the individual investors especially HNIs have the luxury of doing just that, if need be. Currently, markets are primed for perfection and a “goldilocks scenario” where things (including labor markets) should be “just good enough for growth” but not “so good” that the Fed sees it as a risk in its “fight against inflation”.

Potential risks (excluding black swan events, geo political issues, natural disasters etc):

- The Federal Reserve overreaching on the US rate hikes and hence causing a more severe recession vs the current “soft landing” scenario being envisioned by investors.

- Inflation remaining persistently higher for longer due to higher oil prices, commodity disruptions etc.

- High US mortgage rates adversely impacting the residential real estate market and high US interest rates causing financial stress on corporate borrowers and/or distress among financial institutions.

- A growth slowdown in China causing a different set of adverse ripple effects and impacting the already stressed Chinese real estate market.

- The ECB’s actions in Europe could also result in disruptions among the weaker European economies.

- The strength of the USD and a prolonged inflation trend could adversely affect the fast- growing emerging markets (India, South-East Asia)

How Could Investors be Positioned

Some profit taking across various asset classes, at these current “lifetime highs or prices close to lifetime highs” (US equities and residential real estate) is a prudent and sensible thing to do. Holding a “core, good quality asset portfolio” while diligently managing riskier assets and adding to positions without diverging too far away from previous lower acquisition costs. Good high-quality assets bought at “wrong prices” or in a riskier manner than they should be (often involving leverage strategies) can be as disastrous or painful to hold/ own as “bad/speculative” assets. Ones current “financial situation”, in terms of wealth, income potential and timing of expenses etc, is paramount and supersedes everything else (including the analysis in this piece).

Analytics of Various Assets

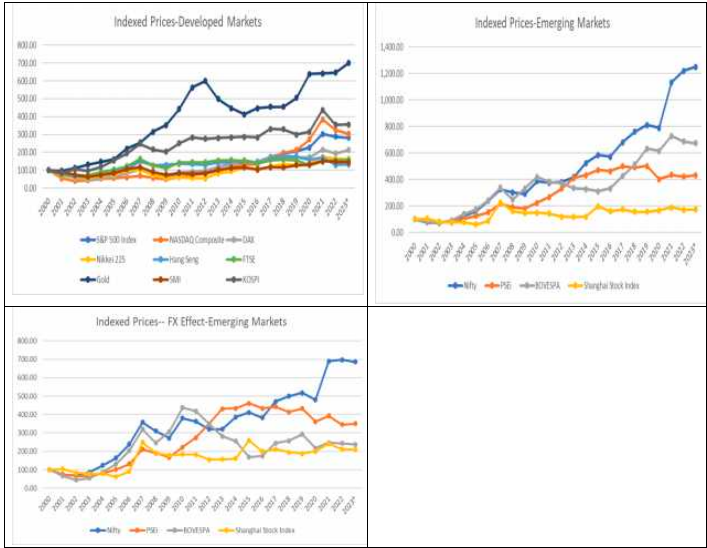

Among the global equities markets, there is a divergence in performance, over a long term, between the faster growing economies and the slower growing economies. USA, Korea, India, South-East Asia have seen explosive growth over the last 20 years in their equity markets and it seems logical based on their economic performances. The European markets and Japan have been laggards across both economic growth as well as equity market performances.

The one exception is China but that can be attributed to how the Chinese economy is structured and the large a role the government and state-owned companies play. The larger Chinese companies tend to use debt financing over equity financing and Chinese investors traditionally prefer to invest in real estate and debt instruments.

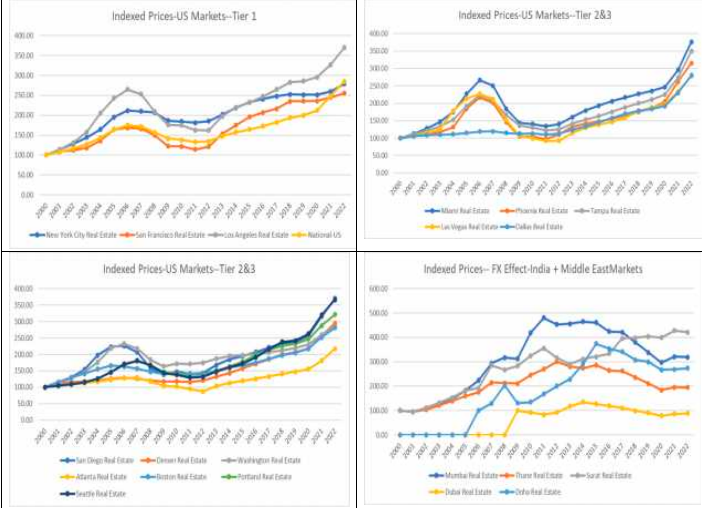

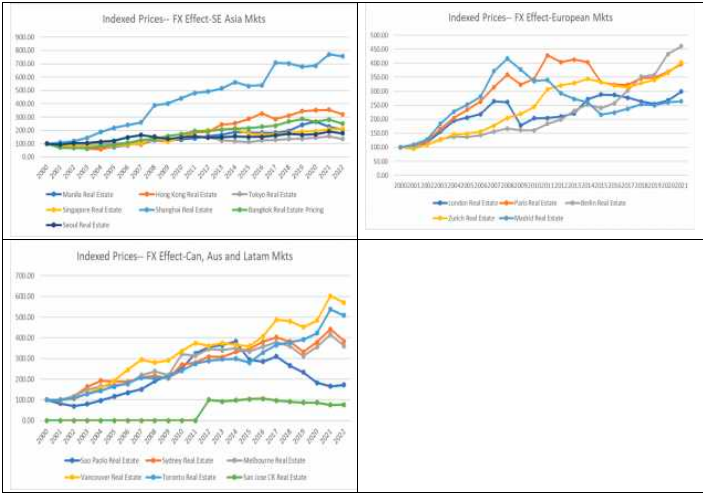

Globally, real estate markets have done well over the last 2 decades, despite the real estate bubble bursting in 2008 and the subsequent global financial crisis. US real estate assets are at their lifetime highs and have overshot the prices reached during the 2006 bubble. Historically, there is a preference to be invested in the marquee global residential markets such as the major European cities. The rise of the “Chinese real estate investor” in the past decade created distortions in real estate markets of Canada and Australia. The Asian residential real estate markets have performed well over the last 20 years but these markets are off their highs. The Asian markets peaked in past decade but over the course of 20 years have generated super returns. The returns of the Asian markets are adversely impacted once the performance of their currency is factored in. Performance of global real estate assets could be viewed through a prism of “USD returns”.

WHAT COULD ONE HOLD OR BUY OR NOT BUY?

Currently, interest rates in the US are at 40-year highs and that percolates to the mortgage markets. Despite strong employment numbers, housing affordability is very low, but non-price housing data does point to lower housing supply. Most major US housing markets are currently priced at their lifetime highs. This makes residential real estate in the US a tricky asset class at this time. It may not be the best way to add “risk” to one’s portfolio. Further, rental yields are coming down, the all equity yields in Tier 3 markets are close to 5% and in Tier 1 markets they are at 1.5%. While yields on 10-year treasury bonds are above 4%. Most HNI portfolios have “core real estate holdings”, but adding more US real estate assets, unless there is a very compelling reason, at this time may not be opportune.

US equities are off their recent highs but the Fed risk is very significant. Further, PE ratios in Sept 2023 for the S&P 500 and the Nasdaq are 23x and 22x respectively. That’s close to average PE ratios over a 30-year period. Additionally, US equities reached their lifetime highs in 2021/2022 and the 3 indices are between 5%-20% off those levels. Further, US equities are currently yielding about 1.5% per year in dividends. This makes the main US equity indices an interesting and viable option. But, there is definite risk to the downside. The “recession” risk related to the Federal Reserve and the labor market could overwhelm equity upside potential. Further, there may be a “small bubble” developing or developed among the Magnificent 7 (TSLA, GOOGL, NVDA, AAPL, AMZN, META, MSFT). The big tech trade is again getting crowded and money has rotated into it from healthcare, energy, banks etc. But, if oil prices go up, interest rates keep rising and a recession risk increases then that rotation will occur in the opposite direction. YTD the equity indices have returned 18% to 33% for the S&P 500 and the Nasdaq respectively. So, adding some risk in the equity markets may be worthwhile, as long as it is adding some index exposure to an already long index position. This is not a piece that is discussing individual stocks. The equity exposure being discussed here is the 3 major indices and if one wants to add additional risk then Russell 2000.

Indian real estate markets have diverged where real estate returns in Tier 2 and Tier 3 markets like Surat have been positive and currently the prices are close to or at lifetime highs. While prices in Mumbai and its surrounding areas peaked around 2015 and prices even now are around 15% below those levels (with currency depreciation it is about 33%). Mumbai, Thane etc seem to be overbuilt and the funk in Mumbai real estate could continue. An additional drag could be due to mortgage rates which are currently in the 9% range. Rental yields across the board in India are anaemic and tend to be in the 2% per annum range, while fixed deposits from banks (akin to CDs) are currently yielding 6% per annum. Hence, it helps to add some real estate from South East Asia (Philippines) to an India position because rental yields in Manila tend to be 5%+. However, the PHP has been depreciating against the USD but that is partly attributable to US Dollar strength over the last few years. Further, the INR depreciates around 3% per year over a longer-term period which creates a further drag on returns. Indian equity markets are at lifetime highs, YTD 2023 returns for the NIFTY 50 is above 10% but the 3-year returns have been around 65%. If one examines returns from the beginning of 2020 then the returns have been close to 100%. Hence, it may be helpful to remain somewhat cautious about adding India or South East Asia risk (equities or real estate), till year end 2023. If some risk in emerging markets is desired then adding small India stock index positions to already existing positions would be the way to go.

CONCLUSION:

From analyzing returns over the last 2 decades or so, its evident that various markets have diverged from each other. Its intuitive and correct to be invested in the faster growing markets vs markets with similar socio-economic or developmental dynamics that are not growing “fast”. The least risky option right now may be to hold cash and see how things play out till year-end 2023. Things are currently priced for “perfection” with risks to the “downside”. If one MUST be “putting some funds to use” then the US equity market maybe an option.