![]() RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

PUBLIC HEALTH ASPECT:

As of Q2 2020, there is unprecedented carnage throughout the planet due to the spread, overwhelming of health care systems and high-mortality rates associated with Covid-19. Adverse health effects of this respiratory virus are significant and the pandemic has affected over 180 countries, infected over 1.3 million people and resulted in the deaths of 70,000 people (April 6, 2020). USA is the worst affected country thus far with New York City bearing the brunt of this dreadful disease. The US has over 345,000 cases and over 10,000 deaths with New York State having over 130,000 cases and close to 5,000 deaths. The EU has also been devastated and has recorded thousands of deaths and hundreds of thousands of infections. Asian countries such as South Korea, Japan, Philippines, India, Iran, China (Covid-19’s place of origin) and others have thousands of cases and deaths.

Currently, there are no drugs or vaccines approved by the FDA to treat or prevent this disease. The only effective method to combat Covid-19, at this time, is aggressive testing to understand where disease clusters reside and then isolate and quarantine people. “Social Distancing” is currently the only known way to prevent further spread and hence “flatten the curve”. Healthcare companies are pursuing clinical trials aimed at Covid-19 vaccines and drug therapies, numerous new diagnostic test have been approved by the FDA.

ECONOMIC, FINANCIAL MARKET AND REAL ESTATE MARKET ASPECT:

As bad as the public health aspect of this pandemic is, there is a huge and devastating economic impact. The current governmental preventive measures imply that entire populations have to remain “at home” and can venture outdoors only for “true essentials”. Basically the global economy has been shut-down for months and this could go on. The first lock-down was imposed in China in January 2020 and continued through February/ March. Throughout March and April 2020, many countries had ongoing lock-downs which are expected to persist. This has devastated many sectors such as airlines, restaurants, retailers, hotels, manufacturing, cruise lines, shipping etc. Employees are experiencing lay-offs, pay cuts, furloughs etc. Additionally, oil prices have collapsed because of lack of demand due to the global shutdown and an oil price war between Saudi Arabia and Russia. The possibility of a recession in USA and possibly globally during 2020 is a foregone conclusion. Economists estimate USA may have no year-over-year GDP growth (2020) and high growth countries such as China, India and Philippines would have sub-4% GDP growth rates.

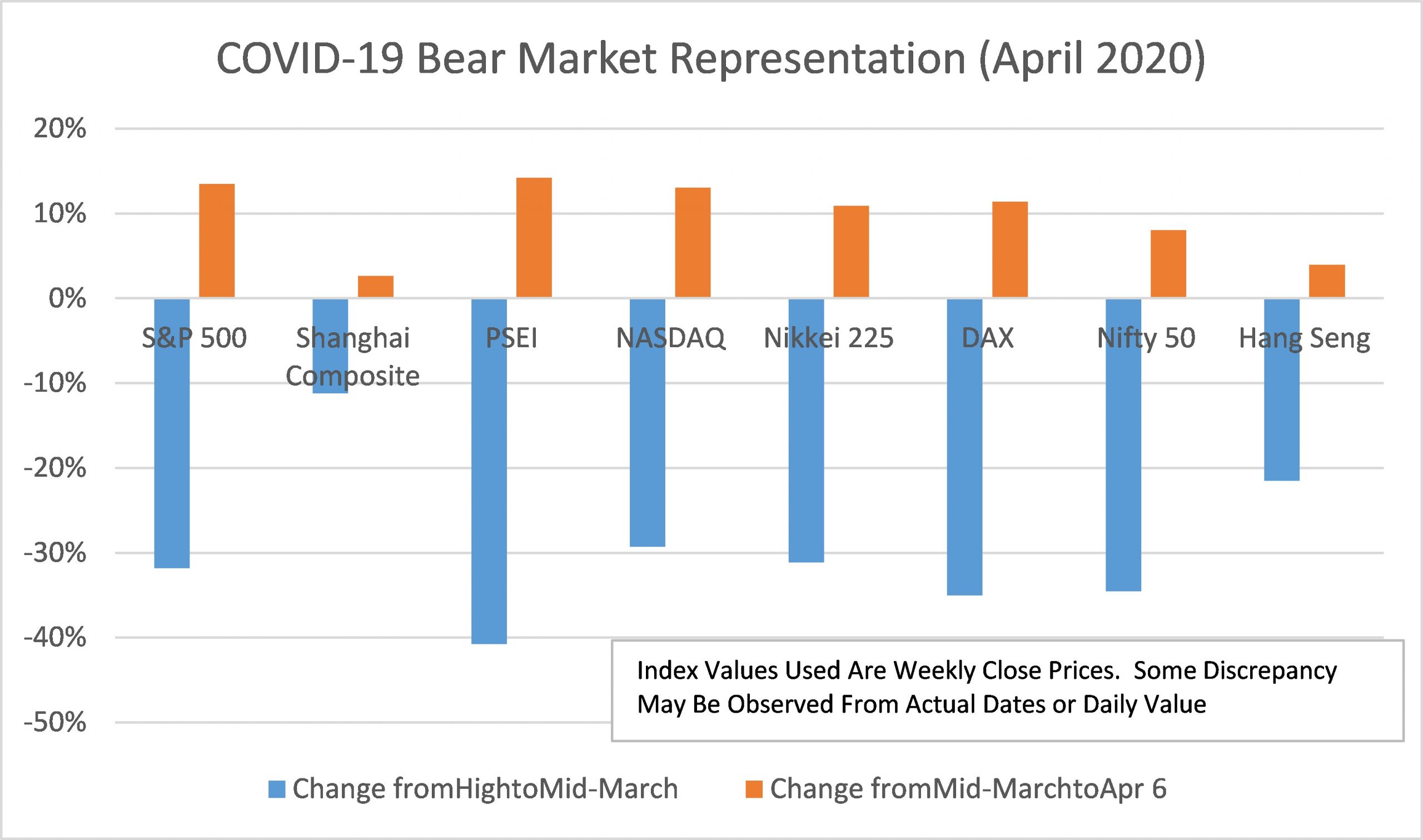

Equity and High Yield Markets: This economic shutdown has devastated financial markets (equity and high yield). Most equity markets globally were enjoying the “longest bull market in history” till January 2020. The major issue was that US equity markets were primed for perfection and any major earnings risk could derail the bull market. The unprecedented shutdown doesn’t just pose an “earnings risk” but has devastated industries and sectors (businesses are expected to report significant losses). High risk of loan defaults and bankruptcy (of highly levered firms) has impacted both high yield and equity markets. Equity markets globally, except China, have lost 25% to 40% from highs reached in January 2020. Till mid-March 2020 (from February highs) all major indices were down, S&P 500 and NASDAQ -25%+, DAX -35%, Nikkei -29%+, Nifty -25%+, PSEi -32%+ (from November 2019 highs), Hang Sang -20% and Shanghai -10%. The developed and emerging equity markets are in bear markets. Prices of High Yield ETFs and Bonds have collapsed, spreads with other bonds have widened, yields have risen and bond ratings have been cut.

The Federal Reserve cut rates by 1% during the covid-19 crisis, two weeks after the March 3 rate cut (50bps), and baseline rate is 0% to 0.25%. The Federal Reserve has also indicated it could “intervene” in debt markets and equity markets, as needed. As of April 9, the Fed announced $2.3 Trillion in additional programs which would include buying multiple bond classes including High Yield Bonds /ETFs.

At the start of the 2nd week of April 2020, equity markets were experiencing “some” positive momentum (could be construed as a “Bear Market” rally). Around April 6, 2020, it seemed that there were gains (could be precarious) in the fight against Covid-19. NYC and many European countries where reporting lower growth in daily death rates and lesser deaths/ infections since the previous day. South Korea reported a significant fall in new infections and China posted no Covid-19 deaths. That coupled with Economic Stimulus packages provided by countries was positively viewed by “markets”. USA has passed an unprecedented $2.0 Trillion economic stimulus package to assist individuals (giving one-time cash payments, increasing unemployment benefits and providing moratoriums on rent/other expenses) and corporations (large and small)—significant sums provided to many industries like airlines, manufacturing companies etc in forms of loans, grants etc.

Loss of pay and job losses has resulted in financial distress for many families in America and globally. USA (Dept of Labor) reported a loss of 700,000 jobs for March 2020. During the first week of April 2020, a record 6.6 million people filed for unemployment insurance.

US Real Estate: Real Estate will not be immune, even before this crisis, many believed that US real estate markets would cool. The prices in residential markets across US cities had risen too quickly and too much (even after accounting for the bubble burst in 2006-2008). Ask prices on many properties were optimistic. Tier 1 and Tier 2 cities like NYC, LA and Miami were experiencing price declines and growth in “time on market”. Tier 3 cities like Phoenix AZ, Tampa FL and Las Vegas NV were experiencing higher prices but slowing growth rates.

The negatives currently faced by US real estate markets are manifold. Early spring activity is slow due to “Social Distancing” and potential financial stress faced by families (future loss of income, job loss, loss of wealth) etc. The overall financial distress and loss of optimism could impact end-user demand. Even though mortgage rates are low and typically would have a positive impact on real estate, the current scenario of low rates is a “rescue package”. Majority of activity, at this time, in mortgage markets is re-financing. Rental income from real estate, at this time, exhibits risk because of governmental measures. This will impact mortgage payments and result in defaults. This would decrease investor appetite to make new purchases. Many markets suffer from low affordability and high prices. All this creates risk to the downside for real estate prices.

Commercial real estate in USA is precariously placed. Large retailers are in distress, restaurant chains are suffering, small stores /restaurants are experiencing an existential challenge. Tenants have informed property owners that rents wouldn’t be paid during the crisis period. There is bound to be pain sharing between landlords and tenants. Commercial real estate prices are bound to be negatively impacted due to loss of revenue and vacancy risk.

Asia Real Estate: In India, real estate prices were suffering even before the Covid-19 crisis. The past real estate bubble (2008-2014) was deflating. Enormous non-performing loans (NPAs) in India’s banking and non-banking sectors were straining the Indian economy, financial markets and real estate markets. GDP growth rates across South-East Asia were slowing down and Philippines was experiencing a slowdown outside of its government spend.

Loss of economic activity globally will have devastating consequences across various markets.

Conclusion—Job Well Done, Needed More Than Ever!

Recovery of asset prices and economic activity will depend on government action, health related and economic/ financial market related. Health risks and detrimental health effects will HAVE to be addressed first. Having a vaccine and drugs which treat Covid-19, in a timely manner, are key needs. The FDA is working with pharmaceutical /biotechnology companies towards fulfilling this public health need. “Flattening of the curve” efforts need to be implemented well (both by governments and people). It needs to be ensured that health systems don’t get overwhelmed, in the short term. Experts believe that a large portion of the population will be infected, the key is to ensure that massive infection numbers do not happen in a short time.

The financial assistance and support provided by governments to financial markets and industries will need to be appropriate and adequate. Once, the recovery starts equity markets will probably “bottom” and then move up. This doesn’t seem to be a “V-Shaped” recovery once economic activity is initiated. The economy is currently at a standstill and getting things back online (supply chains etc) will take time and effort. Getting back to the highs of Q1 2020 would probably take 4-6 quarters once recovery starts. Once economic activity is initiated, markets will get clarity on extent of losses faced by companies and time it will take to get back to a standard situation. After that markets could start their recovery and demonstrate calm on the volatility front (VIXX). The lows reached during Q1 2020 will probably be tested two or more times before equity and high-yield markets bottom and move upwards.

The fate of real estate markets will be tricky. The next couple of quarters will experience price weakening or flattening. Tenants not paying rents in such large numbers will have a detrimental effect on the industry overall. If the overall recovery is managed well and economic activity starts in an effective manner then individuals and investors would feel comfortable about their finances. In such a scenario, real estate could experience a smoother landing and a shorter period of turmoil. This is one of the times when residential real estate around the globe would experience negative results in tandem. US real estate could have some positive momentum post-2021 for a few years, if the recovery is handled well. Real estate in Mumbai has been languishing for some time now and could see some strength post-2021.

Markets, companies and investors are looking for a “strong and adequate” response from governments to avoid the “D-word”! Short-term, the situation is definitely challenging, investors should have enough cash on hand to navigate the crisis. Medium and long term things could improve, if handled well.