![]() RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

RealTMOR Asset Mgmt LLC and RealTMOR Apartment Mgmt LLP

Asset Prices Are Up Now, So What Can Be The Potential Path Forward?

So WHERE ARE WE NOW? All or Most Assets Are At Record High Levels

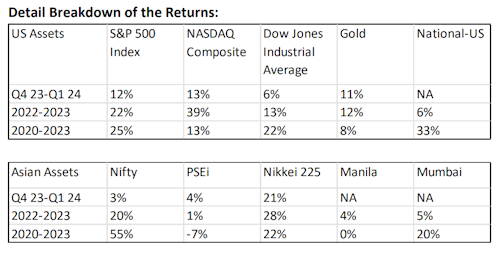

The current investment environment, till Q1 2024, has been exceptionally strong but needs some contemplation going forward. Gold, equity and real estate assets across most markets are at record high levels. So, should an investor continue to add to long positions, maintain current asset positions or do something else? Doing nothing could also entail a risk. Although US stocks have had a negative start for the first couple days of April, 2024. For Q1 2024, the Dow was up around 6% while S&P 500 and Nasdaq had gained almost double that. The midcap Russell 2000 provided strong returns for Q1 2024 and 2022-2023. Significant part of the gains since 2022 in the major indices is attributed to the Magnificent Seven, although in the new year, TSLA has underperformed and positive returns are attributable to mainly six stocks. The midcaps are catching up since 2022 but have had anaemic returns from 2020 to 2023/Q1 2024. It is possible for other sectors (including midcaps), besides technology, to assume leadership. There could be rotation into other areas that could benefit from the strong economy. Currently, healthcare has been a mixed bag while financial services have an overhang in this current high interest rate environment due to risks associated with declining commercial real estate and potential losses in commercial real estate mortgages. Industrials and commodity stocks have some risk associated with them due to the economic slowdown in China the potential “bursting of the real estate bubble in China”. Large Chinese developers like Country Garden and China Evergrande have defaulted on their debt payments and Chinese investors (retail and institutional) are bracing for real estate losses.

The PE ratio of the Russell 2000 for Q4 2023 is around 26x (lowest level since 2020). Average PE Ratios of S&P 500 for Q1 2024 is 26x, (average PE ratio from 1992-2024 is 25x). Hence, even at these prices, the markets may not be “overvalued”. The average forward PE (2025 EPS est) of the Magnificent 7 stocks is around 31x while historic PE is around 45x. The Fed Reserve raised rates 11 times between March 2022 and July 2023, the current Fed Funds rate is 5.33% (5.25%-5.5%) and 30-year mortgage rates are close to 6.9%. Based on current market data (April 2), the probability of a 25bps cut in June 2024 is now at 58% down from 70% in March 2024. Overall, in 2024, 2-3 rate cuts are expected by investors which could result in a 75-100 bps rate cut by year end 2024. Currently, the yield curve is inverted with the 2-year Treasuries yielding 4.7% while 10-year Treasury notes yielding 4.35%. But the yield curve has been inverted for some time. The US experienced a “technical recession” in H1 2022 when the GDP growth was -2% for Q1 2022 and -0.6% for Q2 2022. The impact on the markets was negative (2022-2023), with S&P 500 and Russell 2000 down roughly -17%, the Nasdaq down -30% and the Dow down about -7%. The Fed’s target to begin easing is for inflation at 2% per annum and an unemployment rate above 4%.

Residential real estate markets in the USA are at all-time highs, whether it’s the National Index or a 10-major city composite. The cap gains nationally from 2022-2023 are between 6%-7% while the cap gains from 2020-2023 have been in the range of 30%. The Tier 2 and Tier 3

markets have outperformed the Tier 1 markets both in the last 1 year and over the last 3 years. Even with high rates the residential real estate markets are maintaining their high prices but growth rates have slowed down and sale timelines have increased. Equity markets in Asia are also at record highs. The Nikkei 225 recently hit an all time high and just recently overtook levels last reached at the height of the previous “bubble” in Japanese

assets, in the 1980s and 1990s. The same record was also recently overtaken by Tokyo residential real estate. In India, the Nifty 50 hit record levels and growth from 2020-Q12024 was around 60% but current quarter was flat. While US markets had negative results from 2021-2022, Nifty was flat. Residential real estate prices in Mumbai are still muted, there is some growth but its anaemic for a high growth/high inflation economy like India. Real estate prices in Manila have been flat over the last 3 years, 2020-2023 while they showed some growth, approx. 5%, from 2022-2023. 2024 being an election year in the USA and India creates potential volatility.

Navigating This Environment

Gold prices are up about 10% for Q1 2024 and up about 12% from 2022-2023. But gold prices are up about 8% for the 3-year period 2020-2023. Such price moves in gold mean investors could be thinking of potential “adverse risk events” in the near term. There is significant buying of gold by many governments. Gold prices are at LIFETIME highs. The current environment is very tricky, most portfolios should be having gains. So, navigating/optimizing gains is as tricky as any other maneuver in the markets. There is no doubt that the markets could be prone to a correction from here, there is a small chance that they could even hit bear market levels. There are many risk factors, the biggest being the Fed and its timing related to potential rate cuts. Theres also a risk of a corporate earnings growth rates slowing down and unemployment rates rising more than what investors/ analysts currently estimate. There is definitely a risk of higher rates for longer resulting in asset price deprecation and adversely impacting corporate earnings. So, harvesting a portion of the gains and creating a cash reserve to buy some stocks should the markets dip could be a sound strategy. But, this could also be a “wrong move” if the market continues to move upwards without any pullback. Having said that, TAKING A PROFIT (albeit small) could never be a bad move! Liquidity in the equity markets allows one to trim/add positions, as needed. Real estate being more illiquid demonstrates a challenge to this strategy. For real estate, it is best that investors hold CORE positions and “manage” riskier positions and leverage.

There is no doubt that over the long-term equities and residential real estate in the USA and India are on an upward trajectory. So, being long in these asset classes would be the right thing to do, even while harvesting a small portion of profits. It is never fun to sit through a correction feeling one missed out on the gains previously and now one is in “wait and watch” mode. If adding risk is important then looking at how Russell 2000 has performed over the last 3 years and how its performing now (over the last quarter and last year), it may seem that it is playing catch up to the larger indices. Thus, it may outperform the large caps over the next few quarters. However, mid and small cap stocks tend to be more volatile and hence “riskier” than large caps so, if the markets experience a correction, then the Russell 2000 may experience larger down side pain.

CONCLUSION:

The optimal solution always is case by case and depends on an individual’s financial needs, portfolio, wealth levels etc. But, this be a time to be more prudent than aggressive and harvest some gains while still keeping majority positions in equities while being careful about real estate leverage and risky residential real estate assets. If one wants to add risk then mid-caps could be worth visiting. Going long in the various asset classes at these levels may work if the asset prices move up from here in a linear fashion. But, that is a risky proposition and does not seem the most probable scenario. The risk weighted rewards of such a move may not be optimal at this time.